Create the Right Year-End Check List

The end of the year is a great time to review your QuickBooks Online account and make sure everything is in order. Here’s a quick checklist to help you get started:

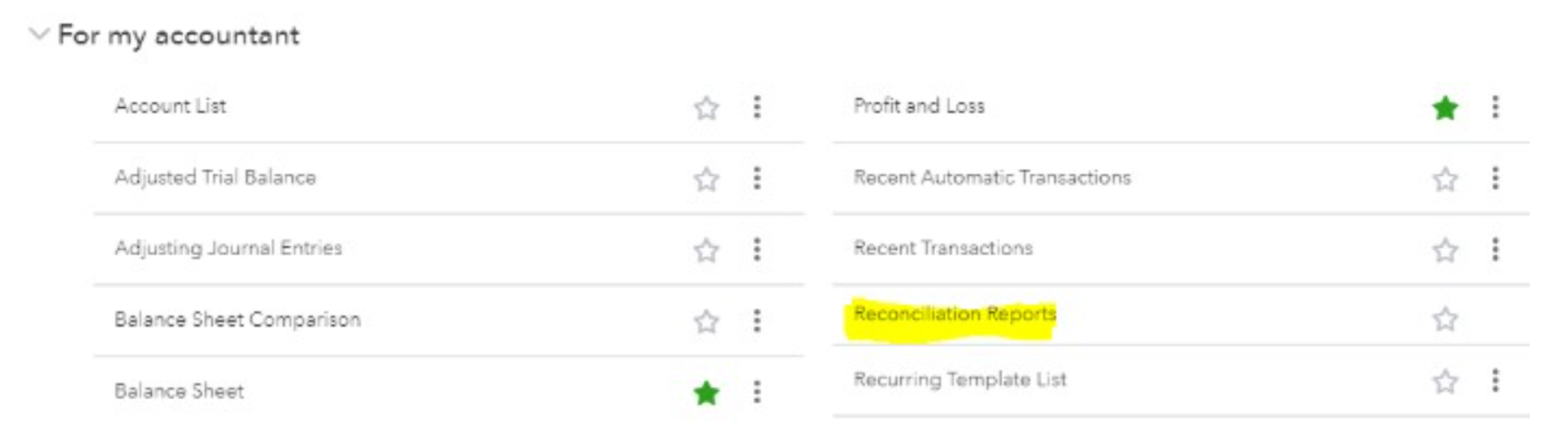

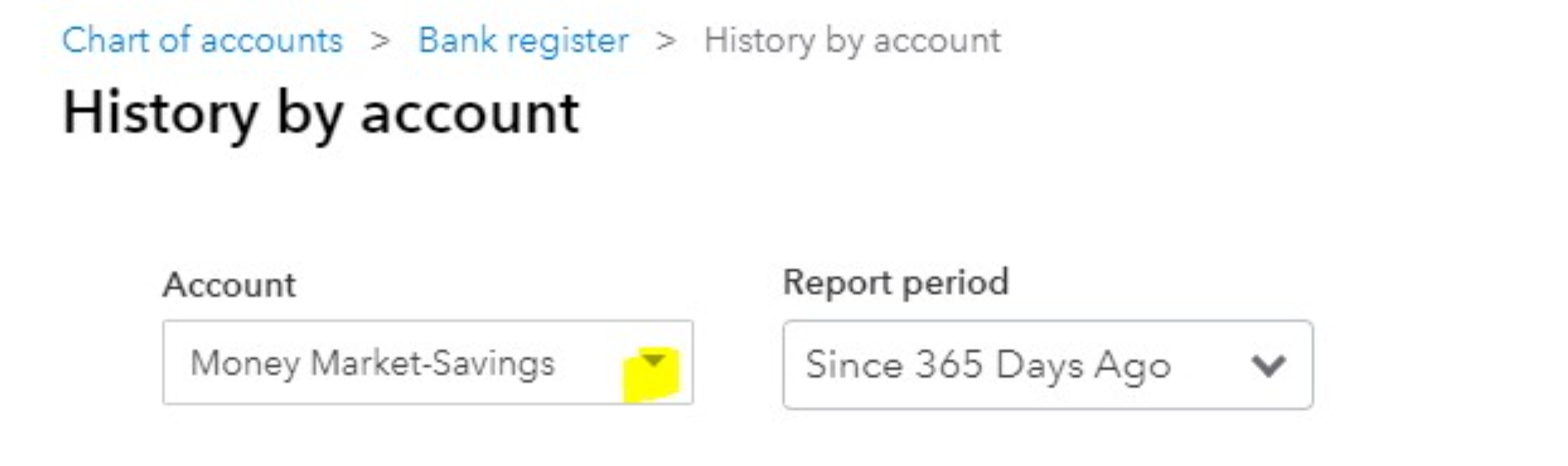

1. Is everything reconciled?

How do I know? Use reports>For My Accountant>Reconciliation Report

Chose each bank account to see when it was last reconciled and if the statements are attached

Review the most recent Reconciliation report. What is outstanding for more than 30 days? Look into those transactions and make adjustments as needed.

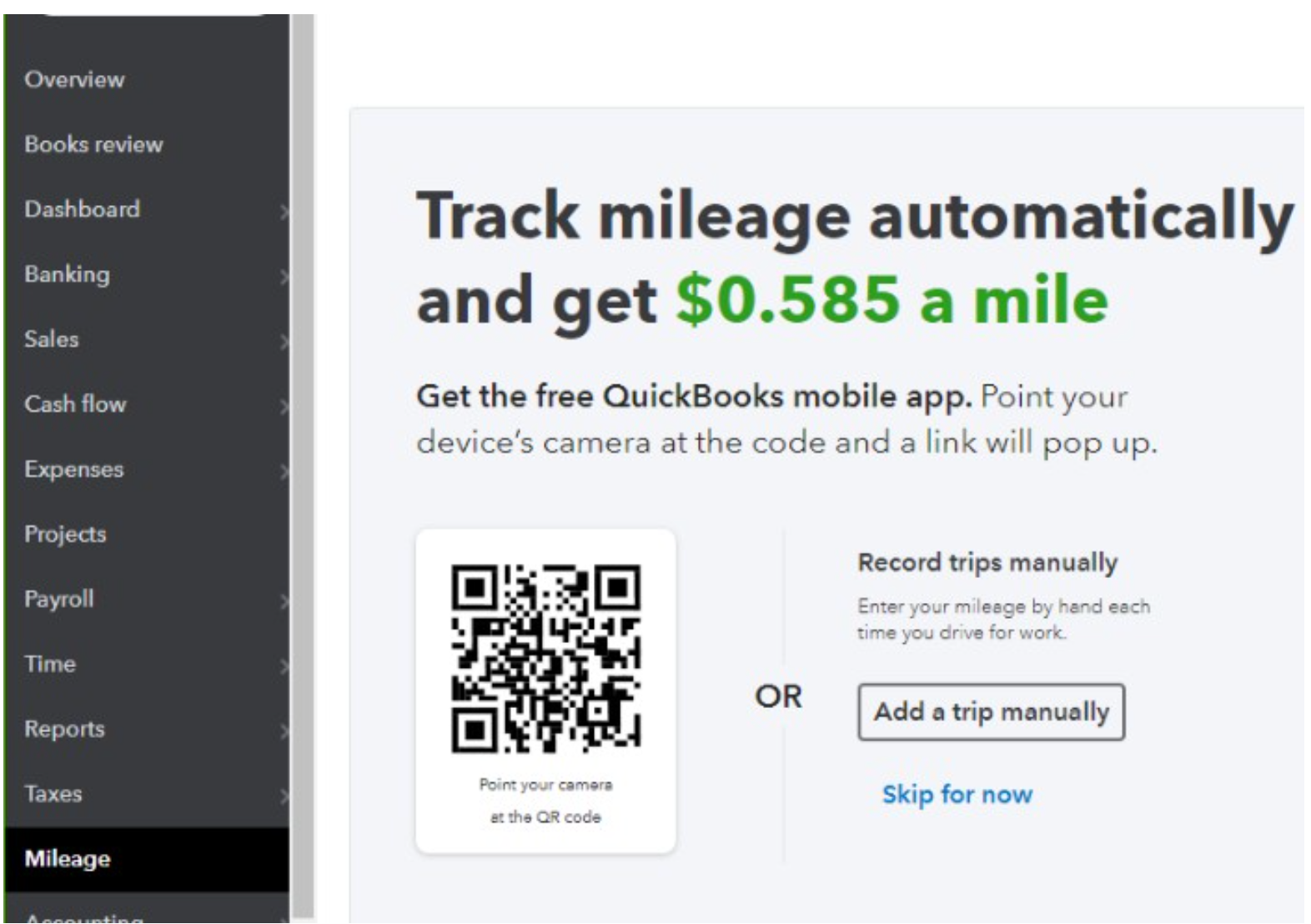

2. Track your mileage.

If you need to have your mileage tracked for tax purposes, do it now. There are plenty of apps that can help you with this and there is one right inside of QuickBooks Online:

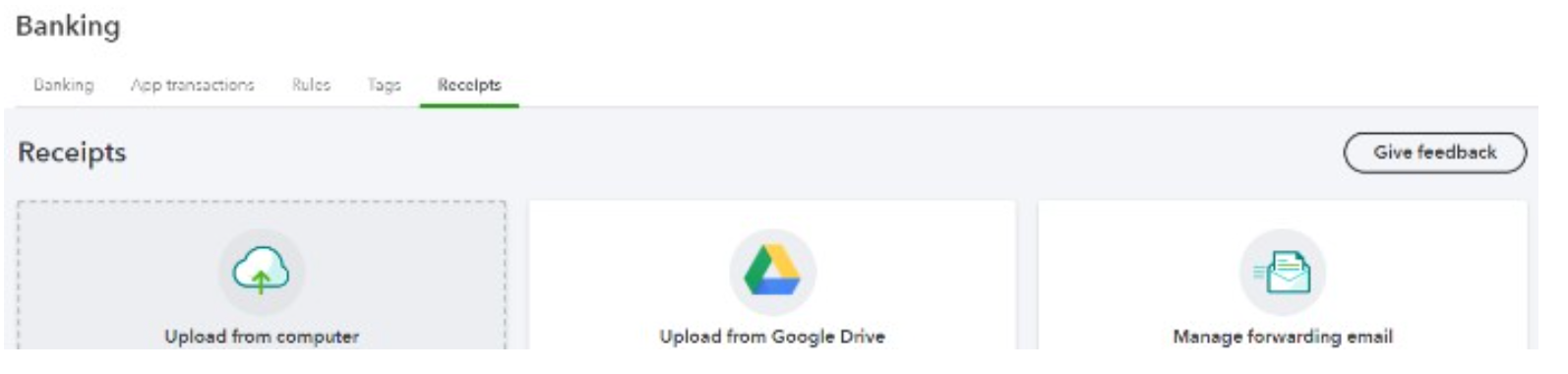

3. Gather your receipts.

Make sure you have taken your paper or digital receipts and have them stored on your computer or inside of QuickBooks Online. There is a receipt capture feature inside of QuickBooks Online that can streamline this process. You can upload receipts from your computer, Google drive or have them sent by email directly into QBO.

Other apps that do an exceptional job of this are Expensify and Divvy. They are very helpful when you have employees who need to provide expense reports and reimbursements.

4. Verify vendor information

It becomes very difficult in January to hunt down vendors for their W-9s. Start now, if you haven’t already by asking vendors for W-9s to keep on file. Make sure their email and physical addresses are up to date, because 1099 forms are sent electronically or mailed. Having done these tasks will make things go smoothly when it comes time to file 1099s to the IRS.

5. Payroll

Are benefits and salaries being calculated properly? You can ask your payroll provider for reports to review and make sure these items are what you are expecting. Start to think about year end profit sharing or bonuses and what those will look like.

We hope this helps you get started on your end of year review. If you have any questions, be sure to reach out to our team of experts. We’re always happy to help!

Our Latest Insight